Not all credit is created equal. The credit bureaus, along with each of their scoring models, all take into consideration the types of credit accounts in a portfolio. While credit mix only accounts for 10 to 20 percent of a credit score, it’s important to familiarize yourself with the three basic types of credit accounts and understand how to manage them properly. The Three Types of Credit AccountsRevolving Credit cards are the most common type of revolving credit accounts. Credit is extended to you on a revolving basis, up until the maximum amount. Once you make your payment — minimum or otherwise — the remaining balance will be rolled over into the next month, subject to finance charges. Installment Mortgages, auto loans, student loans and personal loans are considered installment loans because you are required to pay a fixed sum each month until the loan is paid off. The monthly payment is based on such factors as total amount borrowed, the time period of the loan and the agreed-upon interest rate. Of course, you are free to pay more than the installment amount each month, which can accelerate the term and may trigger prepayment penalties. Open This type is not usually considered a credit account, but it very much is. An open credit account would be one taken out with a utility, cable TV, internet provider or a mobile provider. While not considered credit in a traditional sense, the service provider is expecting you to pay your bill each month, and some providers may run a credit check before initiating service. Open accounts do not usually charge interest — though they might for any unpaid balances — and can appear on credit reports if the service provider reports late payments. Why a Mix of Credit Types Is ImportantHaving a mix of credit account types and paying them off as per your borrower agreements can help demonstrate responsibility to different types of lenders. Banks and financial services companies may consider you less of a credit risk because you’re demonstrating an ability to successfully manage different types of credit and the payment terms associated with them. Indeed, opening and maintaining different kinds of credit, such as a credit card and an auto loan, can help build a credit score. However, because credit mix only accounts for about 10 percent of a credit score, it’s not a good idea to open a new type of credit line simply in hopes of boosting a credit score. Raising Your Credit ScoreBecause each credit agency calculates its own credit score using its own models, differences between reports can produce vastly different credit scores. Most borrowers seek the highest score possible, of course, and one that is consistent. The ability to view, understand and manage your credit is key to putting yourself in the strongest position when applying for a mortgage. Sources: Fico – What Does Credit Mix Mean? TIME – What are the 3 Types of Credit? Experian – How the Right Mix of Credit Can Boost Your Credit Score The post Revolving, Installment and Open Accounts: What to Know About the Three Types of Credit appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/07/12/three-types-of-credit/ Via https://smartcredit1.tumblr.com/post/656546328260853760

0 Comments

Is there a more sophisticated way to build up your credit score beyond paying off accumulated debts every month? Perhaps you need to accelerate the improvement of your credit score to qualify for a personal loan or mortgage. Or you might only have a little leeway to play with, depending on your current financial situation. Although you can’t ‘game’ the credit scoring algorithm as such, you should find that these five strategies help you achieve your best possible score. Make (Your) Credit HistoryYour credit history, the personal chronicle of how often you make loan and credit repayments on time over a period of time, is the single most significant factor in determining your credit score. Yet 62 million Americans don’t have enough credit history on their report to even generate a score. This is called having a ‘Thin File,’ and it means you’re essentially paying the penalty for never having applied for credit. To build your credit history, start early with manageable borrowing on credit cards, for example, and always repay on time. If you can build up a history across a mix of loans, such as car financing, store cards and student loans, you will receive a further boost. You don’t even have to carry a balance on your accounts to increase your credit score, so you can build your credit history without overstretching yourself financially. Check for MistakesYou only get one free credit report a year from each of the big three credit agencies, which means you can be some way behind the actual credit scores that most lenders use. Even more worryingly, your score might not just be out of date. As many as 26% of consumers in the U.S. have at least one error in their credit report. This could be a negligible error, such as a spelling mistake, but for one in five consumers, the error is significant enough to affect their risk profile negatively. That’s why it’s essential to take a proactive approach and check your report early and often for any errors. Keep your Credit Utilization LowIf you are consistently nudging the upper limits of your credit utilization, your credit score can either languish or decrease. Aim to follow the 30% rule instead, paying off your higher balances and interest rates first, paying twice a month if possible, and avoiding minimum payments until your credit utilization is no more than around a third of your available limit. It works the other way too. If you’re a customer who regularly pays on time, you may be able to lower your utilization rate by getting the issuer to raise your credit limit. Tip: Sometimes, the payment due date you see on your credit card statement is actually later than the date the issuer reports to the credit bureaus. That means that even if you pay off your balance, it is too late to affect your score. The solution? Find out what day the issuer reports, and pay before that date. Request Soft Searches for New CreditEvery time you apply for a new loan, the lender will make a search on your credit report. Since ‘hard’ inquiries temporarily impact your credit score, ask the lender to make a ‘soft’ search if possible. A soft search will reveal your current debt, existing loans, and payment history to the lender, but it is only visible on your report to you. A hard search goes into more forensic detail, and it does leave a trace on your report. Typically, hard searches are only necessary when you have agreed to a loan or sign up to a new contract. If the purpose is just to scout out the options, request a soft search only. Monitor Joint AccountsIf you’re wondering how joint checking accounts affect your credit score, bear in mind that regular deposits into (and debits from) a joint account have no impact. Once there are missed payments or unpaid debts on a joint mortgage or loan, however, your credit score could be affected. That’s why it’s important to engage joint account holders in your quest to build your credit score, or close any joint commitments where the other signatory is likely to put your score at risk. Note that being married to someone or sharing the same address does not make you joint account holders. The term applies only to co-signatories of a loan. It’s important to emphasize that there’s no quick fix when it comes to achieving your best credit score. Rather, the focus should be on developing the habits and skills that yield results. Need help? You’ll find the tools you need to track, build and master your credit score here. Sources: Money Advice Service – Next How to improve your credit score Which? – How to improve your credit score Forbes – 3 Ways To Improve Your Credit Score As An Entrepreneur United Financial Credit Union – Looking to Improve Your Credit Score? Follow These 7 Tips Investopedia – How to Improve Your Credit Score Forbes – How To Improve Your Credit Score – Forbes Advisor The post 5 Alternative Ways to Build Up Your Credit Score appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/07/06/altnernative-ways-to-build-your-credit-score/ Via https://smartcredit1.tumblr.com/post/656002760309915648

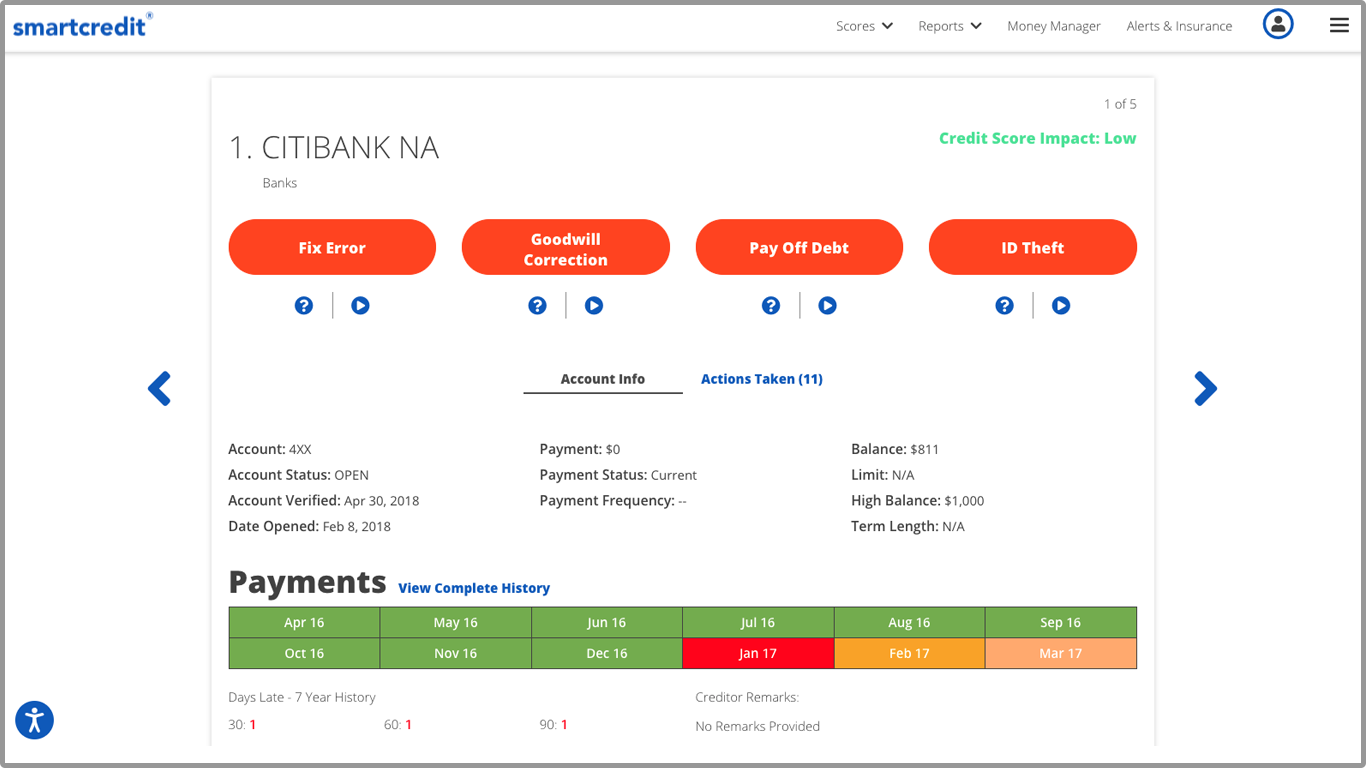

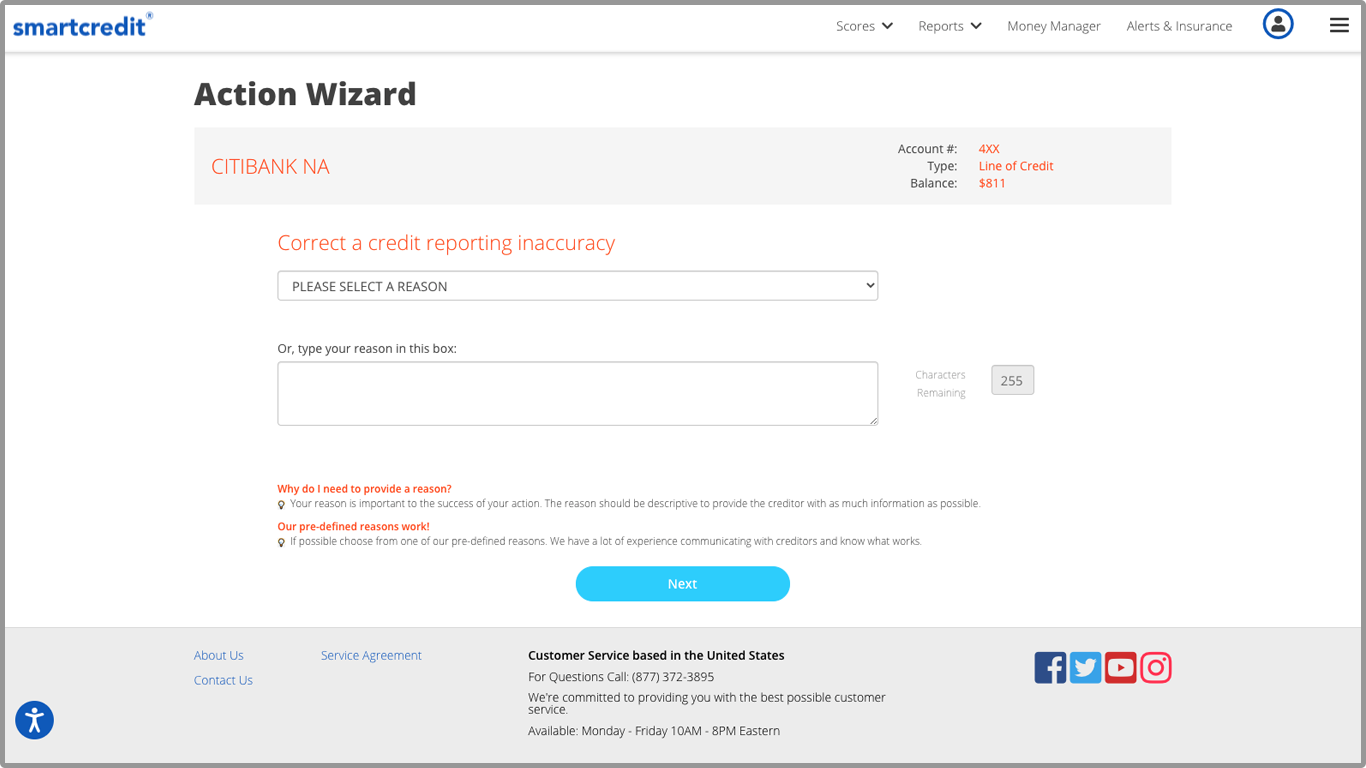

Here’s something most Americans probably don’t know. Up until the FICO® score was created in 1989, people couldn’t actually see their credit score much less do anything to change it. Even worse, they were often denied credit because there was no unbiased standard for evaluating them fairly. Which meant creditors could refuse loans based on someone’s character or even their appearance. Thankfully, the FICO score removed bias from the equation and only focuses on your ability to repay a loan. However, it still doesn’t make it any easier to dispute errors on your credit report. Written disputes and phone calls with long hold times to Credit Reporting Agencies (e.g. Experian, Transunion, Equifax) can be time consuming and frustrating. Of course, knowledge is the most powerful tool you have to overcome these roadblocks. In addition to the solutions covered in this blog, resources like badcredit.org help you better understand how credit works. This includes useful insights on the history of credit scores. The Impacts of COVID-19Not surprisingly, the pandemic has only worsened the challenge of disputing errors. With growing jobless rates and economic insecurity, more people than ever are reporting mistakes on their credit reports. In fact, between September and February of 2021 alone, consumers lodged over 13,000 complaints saying that their disputes were not addressed within 30 days. That compares to just 2,000 similar complaints in 2019, a whopping 550 percent increase All of which compounds the anxiety a lot of people already feel about their credit score. But You’re More Than Just a Number Right?Cliches aside, we all know there’s a person behind each credit score, but it doesn’t necessarily feel that way when you apply for a loan.No matter how hard you try to get around it, your fate is decided by the creditor, and your score plays a huge role in their decision. If only you could take action in a fast and efficient way… Push-Button Power Is the SmartCredit® WayMost of us associate pushing buttons with immediate or fast results.It’s something you can actually do with your finger, a satisfying experience.SmartCredit® gives you that ability. The Action buttons on SmartCredit.com help you send communication directly to your creditors to:

And contacting your creditors directly is what makes our Action buttons so powerful. This completely bypasses the need to contact or deal with the CRAs (e.g. Experian, Equifax and Transunion), and going straight to your creditor(s) is often a much faster and more effective way to get issues resolved. They’re also required by law to contact all three CRAs, so going directly to the creditor can resolve issues on all three of your credit reports.

That’s because all creditors are bound under the Fair Credit Reporting Act by the same rules as the CRAs. So, just as disputes to CRAs must be resolved in 30 days, the same goes for disputes directly to creditors. 2 This approach also helps you avoid the pitfalls of dealing directly with CRAs. For example, CRAs often reject or ignore disputes on technical grounds, but a direct dispute with a creditor prevents that from happening. Additional Advantages of Our Direct ApproachProcessing a Dispute is Faster with Action buttons A Single Dispute to a Creditor Simplifies the Process The problem with writing to three different CRAs? It can result in three different interpretations of your disputes, which means conflicting information is sent to the creditor. Not to mention that each CRA processes disputes at different times, so the creditor may get requests at different times. Key Takeaway: our Action buttons help you send a single dispute to each creditor, so you avoid the confusion and inaccuracy. Permanent Results

Always Stay Informed

Like anything that impacts your life in a big way, it’s best to keep a close eye on your credit score and financial activities. SmartCredit® not only can help you add points to your credit score fast, but also provides a clear picture of your most important information. Our ScoreTracker shows your:

Plus, our Money Manager gives you full visibility of your financial and investment accounts in one convenient place:

Stay informed with sites that bring together the web’s top finance experts, who inform and educate users to make better credit decisions and create a brighter financial future. It’s Only Getting Better

Thankfully, we’ve come a long way since the FICO score was created, but people also need tools that put them in charge. After all, your credit score can actually change your life, for better or worse. WithSmartCredit® you can take command of your credit and finances with the push of a button. We even offer a personalized plan in our ScoreMaster® feature to help meet your future goals. It’s a big leap forward for consumers, and we’re just getting started! Sources: 1 ConsumerReports.org, 2021 2 FTC.org, 2021 The post SmartCredit® Action Buttons: A Big Leap Forward for Consumers appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/06/30/smartcredit-action-buttons-a-big-leap-forward-for-consumers/ Via https://smartcredit1.tumblr.com/post/655459163095302144

Fraud and identity theft are at an all-time high, thanks to the pandemic. Fraud linked to the COVID pandemic has cost Americans $382 million, according to the Federal Trade Commission. As of March 2021, more than 217,000 people had filed a coronavirus-related fraud report with the agency since January 2020, according to federal data. Criminals continue to prey upon vulnerable employees stuck at home, many of whom use unsecured devices and apps and can’t rely on an IT department for help. When they receive a legitimate-sounding offer for help getting another stimulus check or government relief, unsuspecting users might unknowingly hand over their credentials to cybercriminals. The Consumer Financial Protection Bureau fielded 542,300 complaints in 2020, a 54% increase over 2019. What should you do if you find yourself the victim of identity theft? If you believe that you have become a victim of identity theft, there are several steps you can take right away. 1. Call the Companies Where You Know Fraud Has OccurredCall the fraud department of the bank or credit card company immediately and let them know that your identity has been compromised. Do not email them or use digital channels, such as the website chatbot or the company’s Facebook Page — call and request to be connected to the fraud department immediately. You can ask them to close or freeze the accounts, or send you a new card with a new number, depending on their policy. They will also most likely prompt you to change your login names, passwords, PIN numbers or other forms of authentication for these accounts. 2. Place a Fraud Alert and Request Copies of Your Credit ReportsAccording to the Federal Trade Commission’s IdentityTheft.gov website, you are able to place a free, one-year fraud alert on your credit reports by contacting just one of the three credit bureaus — the one bureau you contact must contact the other two. Experian.com/help TransUnion.com/credit-help Equifax.com/personal/credit-report-services Fraud alerts make it harder for someone to open new accounts in your name. By having an alert on your report, a lender or any other business must verify your identity before it can issue new credit in your name. Fraud alerts can be renewed after one year. 3. Report Identity Theft to the Federal Trade CommissionComplete the online form with as many details as you possibly can. You can also call 1-877-438-4338. 4. File a Report with Your Local Police DepartmentWhile local law enforcement officials cannot help you if you were the victim of identity theft online or overseas, they can help you if you were the victim of identity theft locally. Proof of local identity theft can help with an arrest, or aid in assembling evidence for a case. Contact your local police department and file a formal police report. Provide your FTC Identity Theft Report, proof of your identity and address and proof of the theft (bills, notices). 5. Strengthen Your Overall IT SecurityThough the bank or credit card company may have had you change your login credentials, you should also consider changing the passwords for your devices, apps, and even your WiFi router. If you don’t have it already, upgrade your security measures by installing two-factor authentication, so that more than just a password is required to enter your accounts. This can be a fingerprint (or other biometric modality), temporary PIN number, or a number generated by a third-party authenticator app that grants you access — in addition to a password. 6. Scan Your Accounts for Unauthorized ActivityThough you already contacted the bank or credit card company where the fraud originally occurred, scan your other accounts to determine if there has been any unusual activity. This can be especially helpful if you use the same username and password across multiple accounts (which, as a habit, is not advisable). Check for unusual activity even in non-financial accounts, such as online retailers and even mobile food delivery apps in which you have credit or debit card credentials stored. Compromise or misuse can occur in the most unlikely of places. Sources: IdentityTheft.gov – What To Do Right Away US News – What To Do If Your Identity Is Stolen CNBC.com – Covid-related fraud has cost Americans $382 million The post What to Do If You Are a Victim of Identity Theft appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/06/30/what-to-do-if-you-are-a-victim-of-identity-theft/ Via https://smartcredit1.tumblr.com/post/655451631327019008

Only a third of Americans typically check their credit scores each year, but it’s important to know yours even if you’re not currently planning to apply for a loan, mortgage or credit card. That’s because your credit report is of interest to more than just lenders. Fraudsters and identity thieves thrive on dormant or unattended credit reports. Find out why credit monitoring is worth the cost, and how to get the most out of this valuable service. How Credit Monitoring WorksThe task of compiling credit reports falls to three agencies only in the U.S. — TransUnion, Equifax and Experian. Every time you apply for a mortgage, personal loan, credit card, store card or car loan, the lender will request your credit score from one or all of these bureaus. You are entitled to one free credit report from these agencies per year, giving you an annual snapshot of any changes in your credit score or soft and hard inquiries on your report. For a more in-depth overview of your credit score, there’s the option of using a credit monitoring service such as SmartCredit, which usually carries a monthly fee. The advantage is that you gain more insight into the factors that contribute to your credit score and will be alerted to any changes in your profile — notably, hard searches by lenders could impact your score. Credit monitoring is worth the cost if you want to take a more proactive approach to achieving your best possible credit score. Are Free Credit Monitoring Services Enough?Alongside the annual report from the three main credit bureaus, you can also find free credit monitoring services online. While few of us would quibble with a free service, that doesn’t mean there’s nothing to lose. For a start, free credit monitoring services won’t usually pull data from all three credit bureaus, leaving you with an incomplete picture. More importantly, these services offer limited identity theft protection. The stark reality is that fraudsters are relentless and persistent, and they can slip easily undetected through anything but the most robust defences. The Value-Added Services to Look Out for in Credit MonitoringAn annual credit report will tell you where you are now, but achieving your best possible credit score starts with learning more about your patterns and behavior. The best credit monitoring services provide insightful tools to help you manage your money, as well as actionable advice on developing sound financial behavior. They also offer the full picture. With SmartCredit monitoring, you have access to a complete 3B report and scores. Fraud protection is another powerful feature. While no credit monitoring service can prevent fraud, SmartCredit’s $1 million ID Fraud Insurance benefit limits your exposure if the worst were to happen. Key Benefits of Credit MonitoringGiven that 14.4 million Americans were victims of identity fraud in 2018, there’s a compelling reason to go onto the offensive against fraudsters. With regular, thorough credit monitoring, you can block access to your credit report if your identity has been compromised and stop unauthorized credit checks through a credit freeze. Sometimes, it doesn’t even need a malicious attack to impact your credit score. According to the Federal Trade commission, some 25 percent of consumers identified errors in their credit reports. The time to discover errors in your report is not when you are applying for an important loan or mortgage. With regular credit monitoring, you can better manage your score and pursue sound financial planning. SmartCredit offers an industry-leading suite of credit monitoring services to help give you full transparency and control over your credit report. To find out more, start here. Sources Forbes – Credit Monitoring: Is It Worth Paying for? The post Is Credit Monitoring Worth the Cost? appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/06/15/is-credit-monitoring-worth-it/ Via https://smartcredit1.tumblr.com/post/654085105159225344

Many households across the nation continue to face economic uncertainty, so what are the short and long-term effects of missing a rent or mortgage payment? Can an eviction or a missed mortgage payment affect a credit score? Factors That Contribute to a Credit ScoreLet’s first have a look at the factors that contribute to a credit score. While there are dozens of credit models and several different scoring methods used by lenders, the following five factors have become generally accepted as the main drivers affecting a credit score, regardless from which bureau the score was generated:

How an Eviction Affects a Credit ScoreEviction can result from several reasons, such as failure to pay rent or violation of the terms of a lease, such as damaging the property or subleasing without approval. While an eviction might not directly show up on a credit report or background check, eviction-related information can. For example, if the landlord uses the courts to evict you by obtaining a judgment against you, the judgment is a matter of public record and can appear in some background checks. While a background check is not a credit report, an eviction can affect a credit score if your landlord sends any unpaid rent to a collection agency, which will show up on a credit report and will lower a credit score. Like most other types of negative information, the eviction can stay on your credit report for up to seven years. If the statute of limitations for unpaid judgments is more than seven years in your state, the eviction can be reported up until the statute of limitations runs out. How a Missed Mortgage Payment Affects a Credit ScoreA late mortgage payment typically doesn’t affect a credit score until it’s 30 days past due. Logically, a 30-day late payment will have a lesser impact than will a 60-day or 90-day late payment, all other factors held equal. As with any adverse behaviors related to credit, such as a bankruptcy or maxing out a credit card, late payments matter less as they age. For example, a late payment from a few months ago will have a greater impact than a single late payment from five years ago. A late mortgage payment affects those with stellar credit more so than those with lower scores. Simply put, the higher your credit score is before you miss a payment, the more dramatically your credit score will be affected than if your score were just average or poor when the missed payment occurred. Of course, before missing a mortgage payment, it’s best to call your lender and negotiate a short-term solution. In fact, missing a mortgage payment might not have any adverse impact on a credit score at all. Thanks to CARES Act, most mortgage borrowers are legally entitled to a mortgage forbearance for up to 12 months during the COVID-19 pandemic. Credit Simulations and Credit ModelingBecause each credit agency calculates its own credit score using its own models, differences between reports can produce vastly different credit scores. Most borrowers seek the highest score possible, of course, and one that is consistent. The ability to view, understand and manage your credit is key to putting yourself in the strongest position when applying for loans. Borrowers should consider utilizing a tracking tool, such as SmartCredit, that provides monitoring of credit scores and helpful suggestions for actions to increase your score. Such a tool can help individuals understand the dynamics of credit and the impact of open and closed credit accounts on their overall score. Sources The Balance – What Is an Eviction and How Does It Impact Your Credit? The post Missed House Payments and Evictions: How Do They Affect Credit Scores? appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/06/08/missed-mortgage-payments-evictions-and-credit-scores/ Via https://smartcredit1.tumblr.com/post/653450989642366976

If you’re looking to meet additional expenses or expand into new ventures and don’t want to rely on credit cards, one option is to apply for a personal loan. One of the criteria that lenders will take into account is your credit score. Find out what credit score is needed for a personal loan, what else to bear in mind and whether it’s the right choice, depending on your circumstances. What You’ll Need to Apply for a Personal LoanGetting your documents in order before approaching lenders makes for a smoother process and should help you identify the most appropriate lender for your situation. You’ll need the following: Personal loan checklist

Monitoring your credit score with a so-called “soft inquiry” will not negatively impact your score, but once a potential lender makes a hard inquiry bear in mind that this can lower your score temporarily. What Credit Score You Need to Obtain a Personal LoanLenders look at a variety of factors in assessing your risk as a borrower, one of which is the credit score, but also including your age, payment history and current level of debt. As a benchmark, you’ll need a score of 600 or more to qualify for a personal loan, but that is by no means set in stone. For a secured personal loan, you could qualify with a lower credit score if you are able to offer higher collateral, for example, or provide a co-signatory to guarantee the loan. Under the Truth in Lending Act, a lender must inform you of the repayment amounts, due dates, APR, late penalties and so on before you take out the loan, so the process is transparent and you can make a rational decision on the relative risks and benefits of borrowing. How Your Credit Score Influences the Terms of a Personal LoanIf you are able to achieve your best possible credit score above the 600-point benchmark, you should have access to the most generous Annual Percentage Rates (APR) and repayment terms. The options vary on a sliding scale with your credit score. At the lower end of the spectrum, you may still qualify for a personal loan, but you will not be able to take your pick of lenders. The APR might be higher and you may be required to provide more collateral to guarantee the loan. Advantages of a Personal LoanIf you can find a personal loan proposal that fits your current budget and future repayment timeline, the interest rate will usually be lower than borrowing on credit cards. Personal loan interest rates can be as low as 3.49 percent if you have a high credit score, but can go above 29.99 percent for a borrower with a much lower score. The national average is an interest rate of 9.63 percent. Compared to other forms of borrowing, personal loans offer the advantage of a fixed rate for the term of the loan and a clear repayment schedule. That can make for easier debt consolidation, especially if you choose to transfer the remaining balance to a 0 percent credit card. This is only a prudent strategy, however, if you are able to pay off the balance before the end of the grace period and do not make any extra payments or withdrawals with the card. When a Personal Loan Is Not the Best OptionApplying for a personal loan is a less attractive option if your debt to income ratio is already near or above 36 percent. This is the nominal benchmark above which most lenders would see additional borrowing as a risk. Neither does it make much financial sense to take a personal loan for an amount that you already hold in savings or could borrow from friends and family. Watch out for fees too. Lenders can charge up to 8 percent of the overall loan amount to process the application and run credit checks. With the suite of tools from SmartCredit, you can stay on top of your credit score and give yourself the best chance of securing the widest range of options on personal loans. To find out more, start here. Sources: Forbes – 5 Personal Loan Requirements To Know Before Applying The post What Credit Score Do I Need for a Personal Loan? appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/05/31/what-credit-score-is-needed-for-a-personal-loan/ Via https://smartcredit1.tumblr.com/post/652726139420278784 Get credit report comes 24/7 on the web in a couple of clicks on. Smart Credit merely discharged just how the web is actually a piece of excellent information for accessing everything concerning your credit. The net is actually incredible in relation to exactly how you can easily get the relevant information you need to have to take care of practically everything. You may get dishes, commons family products, autos, visa or MasterCard, insurance coverage, home loans, or even any type of popular concern addressed. Therefore, the web is so strong that you can stay at home and never ever leave behind utilizing the world wide web to purchase what you need to have.

The worldwide web is actually the most effective network for credit files, credit rating, and breaking out credit repair work support. You may feel confident you will definitely possess accessibility to what you require safely in a handful of clicks on. If you would like to access your credit report and the outdated manner technique, you would certainly need to wait on get report ahead in the email. I do not understand about you, however, I recognize the email is actually certainly not risk-free any longer. If you may prevent it, you undoubtedly do not desire everything along with your social in the snail email. Along with the surveillance that has actually been actually carried out on the net to get your credit report and credit report secure and safely. Many people do not recognize exactly how handy the world wide web is actually. The web has actually reinvented the means all of us operate and also feature in culture presently. Permits suppose you possess credit concerns, and also you do not understand what to carry out. The majority of people will definitely hunt for credit fixing websites. You will discover that most credit fixing internet sites bill hideous costs for one thing you may do on your own absolutely free. Suppose you were actually to put in the time to carry out some research study. In that case, you will certainly discover that along with a little bit of credit education and learning as well as execution of what you know your credit will certainly enhance its personal. The web is actually similar to your library, it possesses all the details you might visualize. Just how effortless is it to get credit report online?Permit’s think you are actually preparing to get one thing, or even simply wish to recognize what your credit rating are actually. Receiving your credit report is actually thus effortless that a neanderthal can do it. When get your credit report you will certainly require to recognize your credit ratings, usually. Your credit history are going to usually cost you around $30.00 to possess that part of thoughts. It is actually worth possessing feel me. In a concern of a couple of secs along with confirming that you are actually, you will certainly obtain your total 3-1 credit report. Drawing your non-mortgage consumer debt report performs certainly not influence your credit ratings incidentally. Credit Repair on the internetAllow’s say you possess credit problems, as well as you want to begin fixing all of them straightaway. You may locate all type of short articles regarding what the 1st step will remain in the credit repair work method. Along with your credit being actually the solitary essential portion of your economic health and wellness, you can easily feel confident the response performs the internet. In a handful of keystrokes you could be going through a write-up that will certainly concern your circumstance. This is actually the energy as well as ingenuity of the internet today. Got concerns regarding credit? Simply Google it. Get Credit Report For Free as well as From Your HomeThe Fair Credit Reporting Act altered the technique folks obtain economic details. At once, a customer needed to purchase all 3 credit files to access to all of them. With the help of the FCRA every buyer is actually enabled to acquire one cost-free economic claim every 12 months coming from the huge 3 individual coverage organizations: Equifax, Experian, as well as TransUnion. They’re either existing on objective or even being located through error if you’ve been actually moved toward through any person that states you’re certainly not qualified to these documents. You are actually through legislation enabled to view your credit particulars yearly. When the brand-new rule worked, lots of people made the most of the newly found openness in monetary coverage, however equally as lots of folks were actually not aware that a modification in the regulation had actually also happened. Lots of people still spend for all details, fully skipping their once-per-year declaration. When the job is actually carried out online, stating a free of cost declaration of your past history is actually extremely easy. You’ll locate hyperlinks to credit documents spread throughout information as well as details Web web sites that allege to provide free of charge files. Some carry out. Others create pie in the skies. Find an economic coverage Web web site that you’re pleasant along with which comprehends the FCRA properly. Analysis their body for providing your relevant information. Demand additional relevant information coming from the Web website that will resolve any kind of worries you might possess and be applicable if achievable. Review their regards to solution thoroughly. Once you’ve located a Web site that supplies your particulars, it is actually an opportunity to buy the profile. A crucial measure observes this selection. How usually perform you desire to get your files? If you just yearn for one profile each year, that’s your right, yet some individuals would like to take note of their fee discloses more frequently. To accomplish therefore, many Web websites supply year-round cost mentioning solutions that will certainly maintain you approximately day along with whatever on your credit report. The end outcome is that you get a total photo of your credit behaviors and what improvements you need to have to bring in to always keep degree. You can easily get your info online or even offline, through seeking straight apiece of the 3 credit coverage firms. Whether a report is actually sought through email or even through an Internet type, a candidate is actually creating a necessary devotion to maintain their cost score the very best it may be right now and later on. This is just one of the solitary essential actions you will certainly ever before take sustain your monetary safety and security. The world wide web is actually the greatest network for credit documents, credit ratings, and obtaining totally free credit repair work aid. You may relax guarantee you will definitely possess accessibility to what you need to have tightly in a handful of clicks on. Along with the safety that has actually been actually carried out on the net to get your credit report and also credit ratings risk-free and safely. Suppose you were actually to take the opportunity to carry out some study. In that case, you will certainly discover that along with a little bit of credit education and learning and execution of what you know your credit will certainly enhance on its own. Normally when get your credit report you are going to need to have to understand your credit ratings. Taking your buyer credit report carries out certainly not impact your credit ratings through the means. ? Listen to our podcast: https://pod.co/smartcreditcom/credit-monitoring-companies-irvine-smartcredit-com Via https://smartcredit1.tumblr.com/post/652086987439931392 What Should You Know?A provider has to be actually provided as the proprietor of all motor vehicles on California fleet auto insurance, whether it is actually an only proprietorship or even a firm. Fleet insurance might pertain to solitary provider cars and trucks or even many automobiles, depending upon the firm. Attachments to auto insurance, like crash and also detailed insurance plans, will definitely differ. You’re going to need to have business auto insurance if your provider uses lorries. California fleet auto insurance is actually a plan that safeguards your business, and also your staff members ought to an incident or even various other happenings develop entailing a provider car.

Fleet insurance contrasts coming from typical auto insurance in a number of techniques, like being actually only given to companies. Determine what plans appear like in your place through inputting your ZIP code right into our device over. Always keep reading through to find out more concerning fleet plans. What is actually Fleet Vehicle Insurance?Depending on Merriam-Webster. com, the fleet insurance interpretation is actually “insurance through which an amount of vehicles, ships, or even planes are actually dealt with under one arrangement.” Fleet insurance, indicating industrial automobile insurance that deals with a number of automobiles and vehicle drivers, are actually called to shield your organization and workers. You would certainly require fleet insurance for an auto rental business. Providers are actually anticipated to offer a secure workplace for workers. When a provider possesses or even rents cars, despite the amount of, industrial California fleet auto insurance is actually called for to effectively guard the chauffeurs as well as automobiles. Is actually fleet insurance costly? If thus, just how can I spare funds on auto fleet insurance? Your office auto insurance price will definitely rely on what styles of cars you possess in your fleet, and our experts can easily take an appeal at standard auto insurance costs for fleet cars and trucks. Lessening Risks, Reducing CostsFunds Insurance Group may give you along with detailed California fleet auto insurance, giving the deductibles as well as limitations you need to have based upon your direct exposures. Our team likewise gives tactics to assist you in reducing your danger and minimizing the expenses affiliated along with automotive collisions and traumas, featuring carrying out fleet and vehicle drivers’ protection courses. Helpful fleet safety and security course may feature the following:

Our experts will definitely protect extensive California fleet auto insurance and also assist you in making a security course to guard what is vital to your organization. California Auto and also Fleet Insurance SpecialistsWhether you utilize one motor vehicle or even a couple of hundred to deliver flexibility for your staff members, devices, items, or even solutions, it is actually significant to possess the correct industrial California fleet auto insurance in location to secure your company. The VANTREO staff understands the California insurance marketplace and also possesses the competence and also partnerships to guarantee you acquire complete, economical, and also well-considered insurance coverage for your cars. Our team is actually likewise professing, arrangement terminology, and danger monitoring professionals listed below to aid defend your company and its own revenue. What Does Fleet Insurance Cover?Cars and truck incidents occur at bothersome opportunities and also are actually certainly never assumed. Due to this, they were incorporating any individual in your business that possesses a chance of steering an automobile, regardless of whether it is actually a slim possibility, maybe a wonderful suggestion. The insurance firm may certainly not spend the insurance claim if there is actually an incident if one individual chooses one thing up coming from someplace and is actually certainly not guaranteed. California fleet auto insurance deals with the automobiles and also the vehicle drivers that are actually provided on your plan. They perform certainly do not, having said that, cover private products valuable that remain in the autos. Aside from covering your cars and trucks and your chauffeurs, your fleet auto insurance will definitely deal with various other lorries and chauffeurs, along with the residential or commercial property, that a mishap among your vehicle drivers induces loss. There are actually several sorts of plans readily available, therefore seeking your insurance plan to precisely determine what is actually dealt with. Your California fleet auto insurance will certainly not deal with actually the products that are actually being carried, featuring resources, items, and various other things that remain in the lorry. Added security could be acquired to deal with the goods as well as various other points inside your vehicles. Insurance coverage could be purchased for burglary, damages, or even various other reductions. Your insurance solution may assist you in calculating which kinds of plans you require to cover your items, autos, as well as motorists, for your special circumstance.

Is Actually Fleet Insurance Expensive?A lot of variables enter into identifying what the expense of fleet insurance is actually. The lot of autos possesses a considerable impact, as well as they grow older, make use of, kinds, and mileage/value of the cars and trucks in your fleet will certainly affect what you purchase your costs. Obviously, the plan alternatives that you select will certainly additionally influence your fees. Obtaining the appropriate form of insurance for your certain scenario may find yourself conserving a whole lot additional amount of money over time than what you pay out on your costs. How Can I Save Money On Vehicle Fleet Insurance?Truthfully, the leading means to conserve considerable quantities of cash on your California fleet auto insurance strategies is through tapping the services of chauffeurs that possess tidy and risk-free driving reports. Including vehicle drivers that possess a bad driving report, also among all of them, can easily elevate your fees through as much as 10% or even more. Considering that you are actually covering several automobiles, this form of cost boost can easily amount to considerable volumes of the excessive loan being actually devoted. Some providers opt merely to enable individuals in the firm along with the most effective driving reports to steer, conserving a fair bit of cash while doing so. Yet another best technique to conserve funds is actually by packing your auto insurance and various other sorts of plans. Suppose you are actually buying a life insurance policy, company insurance, or even some other types of security. In that case, you may receive the plans coming from the very same firm for notable cost savings. Added savings may be on call for possessing points like GPS units put up in your lorries, and this could be a reasonably cost-effective technique to spare an amount of money, as well as may additionally aid you to take note of your business’s autos. If any kind of is actually taken, they may additionally aid outline a motor vehicle in your fleet. Away from these others and price cuts, transforming and upgrading your plan may bring about discounts. If you decide to component means along with pair of automobiles, for instance, make certain to allow your insurer to recognize them straight away. There is actually no explanation to purchase cars that are actually certainly not had due to the provider any longer. Your industrial auto insurance expense is going to rely on what kinds of lorries you possess in your fleet, and our team may take an appearance at basic auto insurance fees for fleet vehicles. Whether you utilize one lorry or even a couple of hundred to give a range of motion for your staff members, devices, items, or even companies, it is actually essential to possess the correct business fleet auto insurance in spot to shield your service. California fleet auto insurance deals with the lorries as well as the vehicle drivers that are actually provided on your plan. In enhancement to covering your autos and your motorists, your fleet auto insurance will deal with various other cars and chauffeurs, as effectively as the home, that a mishap one of your motorists creates a loss. Your fleet auto insurance will certainly not deal with actually the products that are actually being carried, featuring resources, items, and various other products that are actually in the motor vehicle. ? Listen to our podcast: https://pod.co/smartcreditcom/irvine-ca-financial-service-get-credit-score Via https://smartcredit1.tumblr.com/post/650905868376948736

Financial planning can look a lot different in your 30s than in your 20s. If you’re approaching your 30s, chances are that by now you’ve already learned a thing or two about financial management. Though it’s never too early to start planning for your financial future — and it’s never too late to start a new career path, either — by the time you’re in your 30s, you should begin making even smarter financial moves. We’re here to help get you started on the right foot. 1. Build Your CreditThe first piece of financial advice for your 30s, if you haven’t done so already, is to build your credit. Building your credit can take several years, especially if you’ve had some financial setbacks or struggles in your 20s. Having solid credit will open up more financial opportunities for you, like purchasing a house or getting lower interest on a loan to start a business. Credit can be used in multiple advantageous ways — all you need to do is get your credit score up. Credit monitoring tools like SmartCredit can help create a plan to achieve your best possible score, all in one easy app. But here are some basic principles: Get rid of debt Your 30s is a good time to start getting rid of the debts you have. While there are some “good debts” — having a mortgage or car payments — start to tackle credit card debt if you have it. Not only will this put more cash in your pocket every month, take the burden of debt off your shoulders and lower your debt-to-income ratio, but it will, at the very least, boost your credit. Utilize promotions and offers Taking out more credit cards wouldn’t exactly be great financial advice for your 30s. However, if you are receiving promotions for 0% balance transfers for a new credit card for up to 18 months, or you’re given the offer to consolidate your debt with a lower interest rate, you might want to take advantage of these opportunities. Refinance Interest rates are at an all-time-low right now, and your 30s could be a good time to refinance if you already have a student loan, car loan or mortgage. Of course, you should always read the fine print and make sure you’re getting a good deal and not a bad one. All things considered, this could save you some money in the long run. 2. Think About Your Budget, AlwaysAt this point in your life — even if you’re still in school or thinking about what career you want to pursue — you should at least have an idea of what type of life you want to lead. Do you want to travel often or do you want to buy a house (or both?). Do you want to have kids someday or are you not even ready to make that decision yet? Do you want to have a collection of nice luxury cars or a minimalist life? Whatever it is that feels right for you (and yes, this can change still as you get older), you should be aware of what type of budget you need to have — both on a regular, everyday basis and for the near or far future. A budget can certainly change as you earn more money and/or your preferences change, but adults in their 30s who are wise with their finances will always pay attention to their budget. Downsize and consider what’s important Some people spend their whole 20s accumulating a lot of stuff and reach their 30s only to be asked by their parents to move out any childhood items from their home. It may not seem like a smart move financially to get rid of things that you spent money on. But, this can actually help you be more mindful about “stuff” and spending in your future. 3. Have a Reliable Emergency/Savings AccountThese days, many financial experts are advising people to invest their money instead of letting it sit in their bank accounts. While this is valuable advice to some extent, you have to at least have a reliable emergency fund/savings account before investing the rest (if that’s your choice). This fund should have anywhere between three months and six months of living expenses, to get you through hard times if you lose your job or have a sudden medical emergency (though, you could have that separate, too). Always replenish this account if you have to tap into it, because even if you’re in a salaried position by the time you’re in your 30s, you never know what can happen. You wouldn’t have to start back at square one when it’s time to start really building a financial foundation for your future. 4. Invest Your MoneyThese days, everyone is talking about investing, investing, investing. If you’ve just managed to create a nest egg for yourself, it may feel scary to take that money out and invest it. But once you feel secure enough with an emergency fund/savings account, then you can begin to look towards investments and assets for your future. Real estate Historically, real estate has always been a popular and reliable investment choice. As homes typically appreciate in value, buying one in your 30s means that by the time you’re in your 60s, you’ll have something to either live in or sell for, hopefully, much more than you paid for it. If you plan on doing this, then you will need some investment money that will go towards your down payment, closing costs and other costs associated with home ownership. Talk to a loan officer to see what your options are. Retirement funds Not all, but many employers will have you registered with a 401(k) or similar pension plan. Start paying into this, especially if your employer is going to match it. Additionally (or, if you don’t have that option), you can open up a Roth IRA account and add up to $6,000 a year. There are many benefits to putting money into a Roth IRA, and the sooner you start paying into it, the better prepared you’ll be financially for your retirement. Stock market Another financial move in your 30s is to begin investing in the stock market. There’s so much information out there about how to go about this, as well as apps like Robinhood and Acorns that can help you easily learn the ins and outs of investing in stocks. Just do so with caution — if you’re not experienced, you don’t want to end up losing a lot of your money. Your future children or your children’s future Whether you already have children or you’re planning on having children in the future, your 30s could be a good time to start saving for them. From baby expenses to summer camp fees to a college fund, savings for children will look different for everyone, and there’s no right or wrong way to go about it. Just do what makes sense for you. 5. Prioritize and Revisit Insurance PoliciesBy the time you reach your 30s, chances are you’re already paying insurance for several things in your life. But, now could be a good time to start thinking about things like a life insurance policy for yourself as well as your partner. It could also be a good time to see if you can start getting better rates on your other insurance policies, too. Usually, being in your 30s can look good in the eyes of insurance companies (assuming you’ve given them no reason to up your rate). 6. Meet With a Financial AdvisorIf you’re serious about making smart financial moves in your 30s, then you can consider meeting with a financial advisor. A financial advisor can sit down with you and help you come up with financial goals for your 30s and your future, assess your finances, and help you make the best choices to help you reach those goals. A financial advisor can also invest your money if you trust them to do so. Sources: WellsFargo – Saving for an emergency Forbes – 15 Best Investment Apps CNBC – Here’s why you should buy life insurance when you are young The post The 6 Best Financial Moves You Can Make in Your 30s appeared first on SmartCredit Blog. from SmartCredit Blog https://blog.smartcredit.com/2021/05/11/financial-planning-in-your-30s/ Via https://smartcredit1.tumblr.com/post/650868922276560897 |

|

RSS Feed

RSS Feed